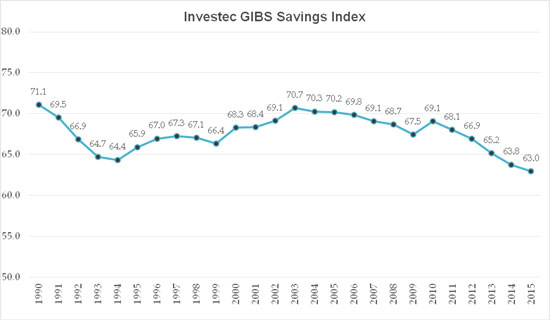

These 2015 scores are a far distance from the required score of 100, which represents the savings structure of economies that produce high rates of sustained and inclusive economic growth. This data emphasises the extent of the SA savings deficit and the large gap that exists between planned economic growth of 5.4% per year, as per the NDP, and the ability of the South African economy to fund that growth.

Low business confidence has far-reaching effects

Insights derived from the latest savings index data, when married with the current economic environment, flag some key trends. René Grobler, Head of Investec Cash Investments explains, “Business confidence levels are very low which will certainly have a knock on effect on fixed investments and the rate of investment is crucial in terms of fueling the economy and creating jobs. According to latest figures, the rate of fixed investment is at around 20%, while we require a rate of 30%. So we’re only two-thirds of the way there and that is really concerning.”

Businesses operating in environments with high levels of uncertainty tend to keep a higher level of cash reserves, which would mean that in this interest rate environment, they will be earning higher returns. They will however need to deploy these funds at some point in order to provide the right returns for shareholders, according to Grobler.

Good news for savers

A positive development, however, has been the hike in interest rates, with the latest MPC meeting last month taking the repo rate to 7%. While this bodes well for savers thanks to a higher return on their cash investments, we know that South Africans haven’t been good at saving. In fact, as Grobler points out, we’ve been good at accumulating debt. “The debt to income ratio for consumers in SA stands at about 77%. This means the higher interest rate will actually translate into higher debt servicing costs, which will have a knock on effect on income levels. We can see this coming through in the environmental factors in the index, evidenced by a drop in per capita income,” she says.

SA’s fiscal status still regarded positively

South Africa’s fiscal status and in particular monetary management remains really impressive, as Dr. Adrian Saville, Professor in Economics and Competitive Strategy at GIBS and Chief Strategist at Citadel explains, “What we see is sensible fiscal policy underpinned by robust monetary policy – and the latter pushes through in the index in the form of a very high real interest rate. So here we have evidence of the SA Reserve Bank being on the front foot – as the country’s central bank has raised the key interest rate in anticipation of domestic inflation and in anticipation of the Federal Reserve. The SA Reserve Bank is ahead of the curve, so to speak.”

Positive indications include cumulative gross savings as a percent of GDP. However, according to Saville, this is explained by stalling GDP growth rather than an outsized gain in cumulative savings. In addition, capital stock per worker, which is an important driver of productivity continues to show steady gains, rising from a score of 33.9 for 2015Q2 to 34.3 for 2015Q4. This remains some way below the capital invested per worker in the so-called Savings Stars – countries that have sustained an average economic growth rate of 7% per year for 25 uninterrupted years or more – but does underpin the potential for productivity gains in South Africa’s workforce.

“Productivity is a great approximator for competitiveness because the only way to build truly competitive companies, industries and countries is by improving productivity,” adds Saville.

“The trend in the index emphasises that all stakeholders in society need to pay attention to the very real deficit that we have in our savings environment. The call to action is not just for the policymakers to give us more tax breaks. We need to urgently find ways to create more income and jobs and being responsible and prudent about spending or saving money that is created. It’s about resisting instant gratification and instead, thinking about the future,” concludes Grobler.